Like Bananas - Brugel's WNWN

What's Now What's Next - 2025-19, July 3

This Week:

1. Not Close

2. Like Bananas

3. Factors

4. What Matters

5. Huh?

Weekly Summary:

Another risk on week. Credit spreads eased. Volatility flatlined. Interest rates were benign. Stocks continued the relentless move higher. Bitcoin toyed with the idea of going down but then recovered. Oil recovered some of its recent losses, but still ended in the 60’s. All in - clear skies heading into the long weekend.

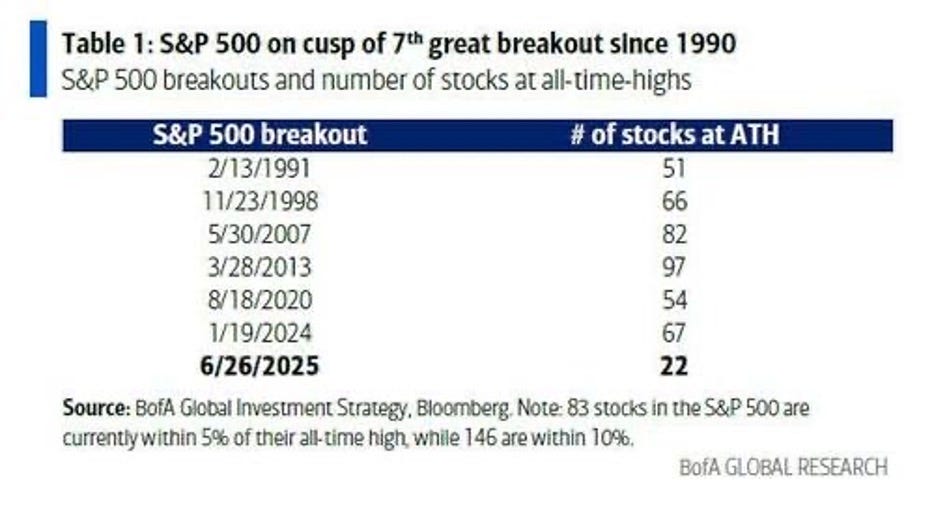

Not Close

Not even close. By far the lowest number of S&P components at ATH as the index hits ATHs.

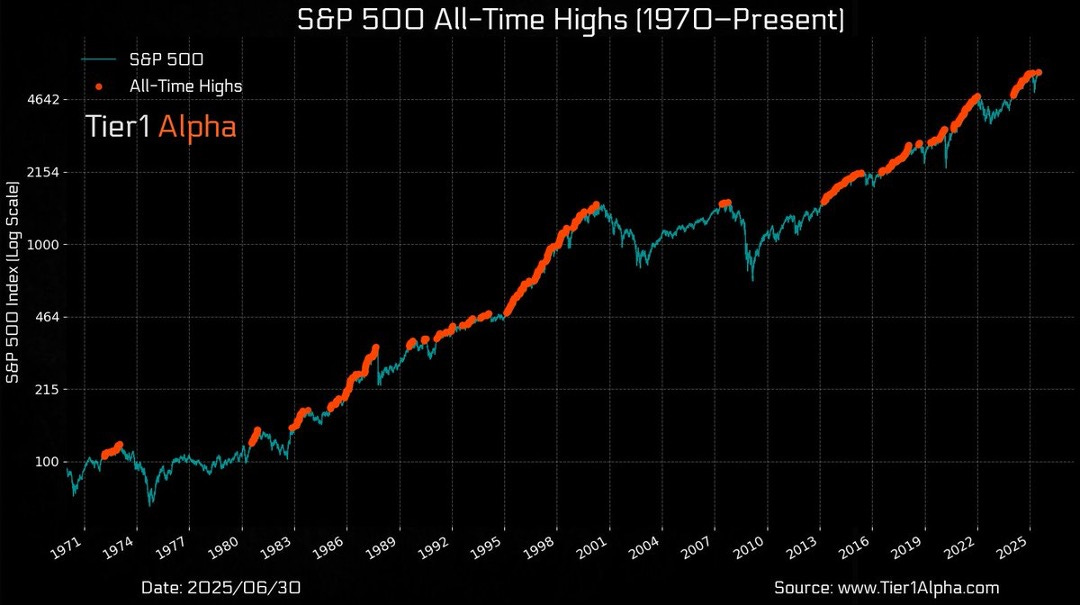

Like Bananas

All-Time Highs are like Bananas. They come in bunches. 90% of ATH’s have come within 5 days of each other. Case in point, the S&P 500 had 3 All-Time closing highs this week, and there were only 4 trading days.

Factors

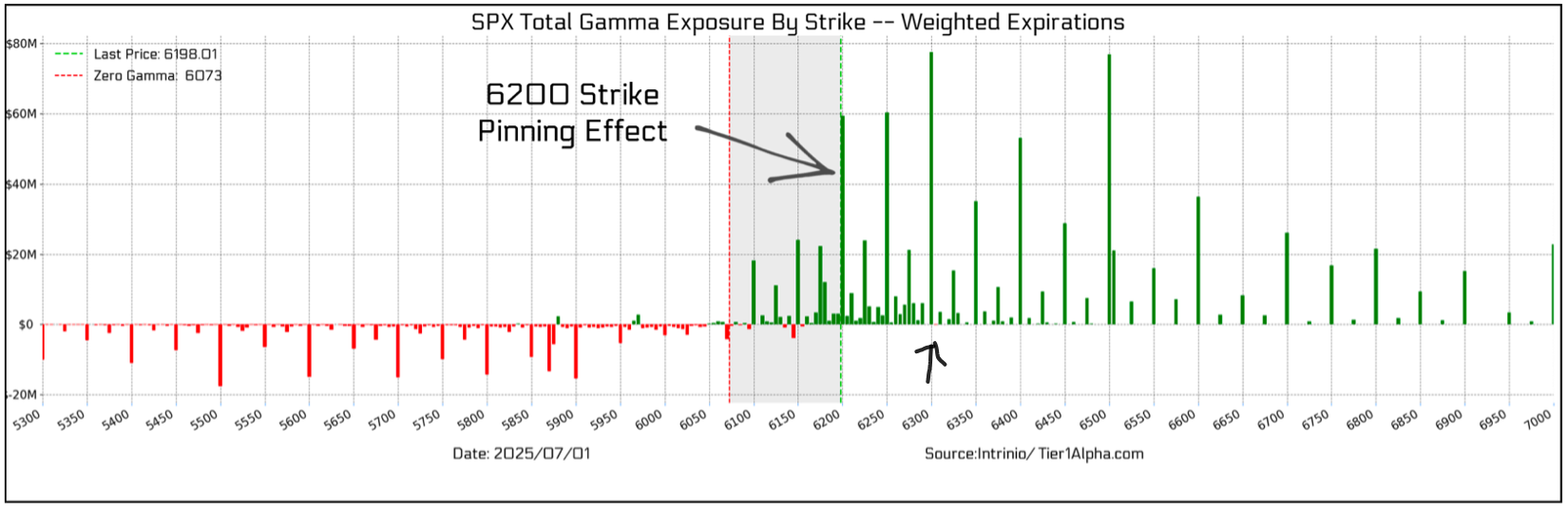

On Tuesday July 1, we saw some notable style divergences. Investors are much more focused on factor exposure than individual company fundamentals. Factors like industry, capital structure, size, debt level, and growth profile are more critical than idiosyncratic company issues. On Tueday it showed up in the “Momentum” factor with several highfliers getting slammed (OUST -11%, AEVA -24%, NBIS -9%, OKLO -8%). 76% of S&P 500 companies were up and average of 2%, but the index closed down 0.1%. Some may interpret that move as a sector rotation, but the more accurate explanation lies in the market structure, where a pinned index clashes with idiosyncratic risk. When Apple and Nvidia are up big to keep the index in check TSLA, MSFT and META are down. In this chart you can see the levels of dealer Gamma exposure at various SPX strike prices. Index levels will often pin at/near a key strike. With my crudely drawn arrow below you can see 6300 is the strike with the most dealer gamma. The index closed at 6280. Dealers will do what it takes for the index to close at/near the “right” strike. The levels of the underlying stocks (MSFT, NVDA, etc.) will be adjusted accordingly.

What Matters?

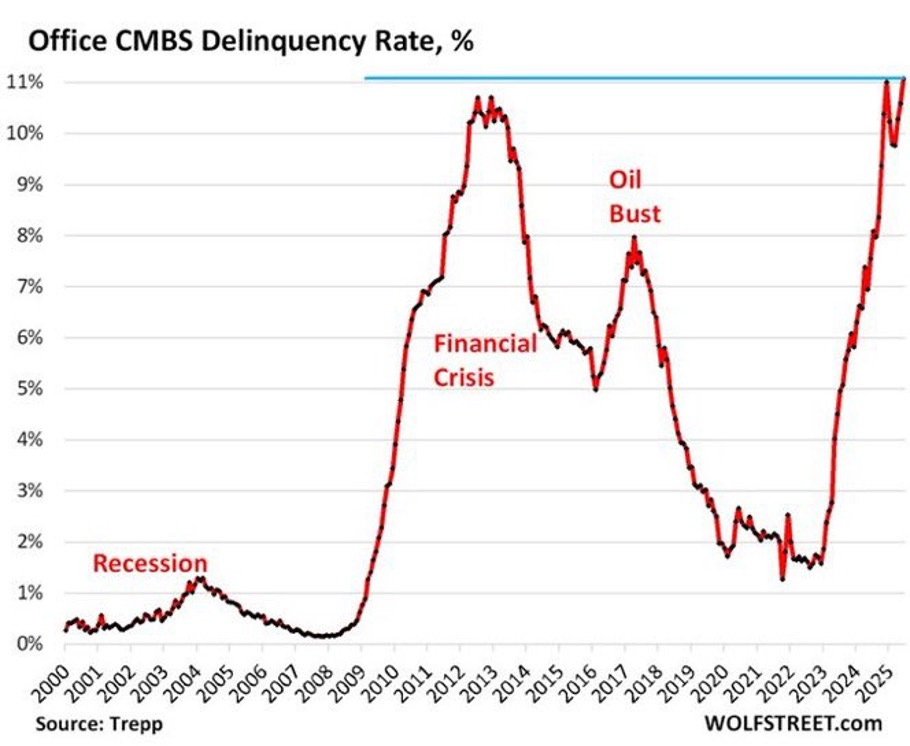

Commercial Real Estate (CRE) is in turmoil. One out of nine loans are bad, and landlords are simply giving back the keys. Vacancies in several big cities are above 30%, leading to significant RE tax shortfalls. Boston is projecting a $1.7B tax shortfall. Companies are downsizing real estate needs as remote work is now a permanent part of the landscape. There are $2 Trillion of CMBS loans coming due by 2027. From bartenders to bus drivers there is a big cadre of workers that depend on those buildings being full. This is an important socio-economic issue confronting the U.S.

Does this matter to the stock market and 401ks? Not even a little.

Huh?

@HenrikZeberg on X highlights the “Piper Sandler Recession Signal”. The signal only tracks the level of unemployment and it’s simple: when the 3-month simple moving average moves above it’s level from 12 months earlier the signal triggers. In the past 60 years this has occurred seven times and recessions have followed each time. It last occurred in 2020 and we had the briefest of recessions. We have not had a “real” recession in 16 years. The index has triggered again. If a recession does follow this will matter for stocks and 401k balances.

What’s Next

1. America’s Birthday celebration. Happy 4th of July!

2. Mortgage data and Fed minutes on Wednesday 7/9

Action items

1. Stagflation on the horizon. Utilities, Energy and Tech do best in this mode. Precious metals and Bitcoin also do well in stagflation.

Please feel free to call me if you would like to discuss any of this and how it might impact you personally.

Stay well!

Eric

703-307-5253

This newsletter contains general information that is not suitable for everyone. The information contained herein should not be construed as personalized investment advice. Past performance is no guarantee of future results. There is no guarantee that the views and opinions expressed in this newsletter will come to pass. Investing in the stock market involves the potential for gains and the risk of losses and may not be suitable for all investors. Information presented herein is subject to change without notice and should not be considered as a solicitation to buy or sell any security. Any information prepared by any unaffiliated third party, whether linked to this newsletter or incorporated herein, is included for informational purposes only, and no representation is made as to the accuracy, timeliness, suitability, completeness, or relevance of that information.